FCA ESG integration in UK Capital Markets

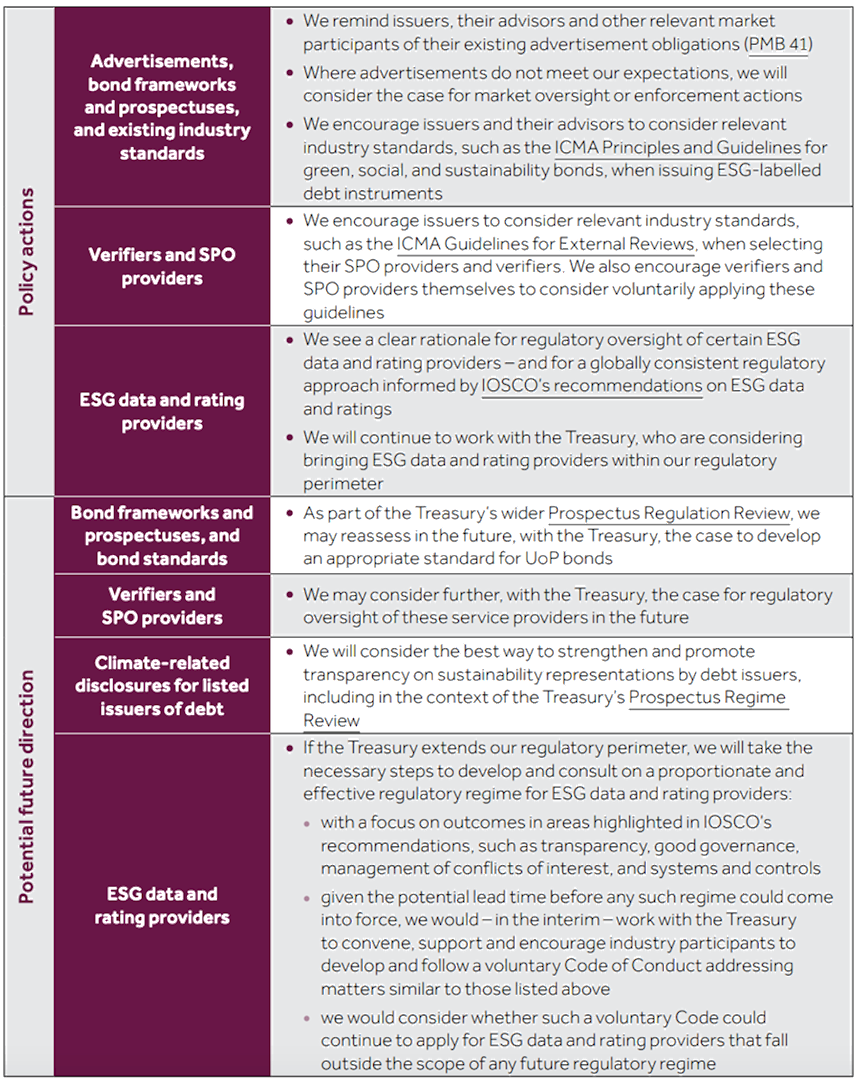

On 24 June the Financial Conduct Authority published paper FS22/4: ESG integration in UK capital markets summarising feedback to its discussion chapter (in CP21/18) on environmental, social and governance (ESG) integration in UK capital markets and setting out its potential next steps. The paper sets out a series of policy activities that the FCA may undertake in the future, connected to its strategy published earlier in the year.

The FCA also published Primary Market Bulletin 41, further elaborating on the responses to the consultation, with a particular focus on ESG-labelled debt instruments. In particular, the FCA:

- Encourages issuers of ESG-labelled Use of Proceeds (UoP) debt instruments to consider voluntarily applying or adopting relevant industry standards, such as the Principles and Guidelines that the International Capital Market Association (ICMA) has developed for green, social, and sustainability bonds;

- Reminds issuers, their advisors and other relevant market participants of their existing obligation to ensure any advertisement is not inaccurate or misleading, and is consistent with the information contained in the prospectus; and

- Encourages issuers and their advisors to consider verifiers' and assurance providers' expertise and professional standards, and to engage with second party opinion (SPO) providers and verifiers who adhere to appropriate standards of professional conduct, such as ICMA's Guidelines for External Reviewers.

Key Policy Actions and Potential Future Direction (Source: FCA)

At the same time, the Financial Conduct Authority (FCA), revealed that it is extending the process to introduce sustainability disclosure requirements for asset managers and ESG labelling rules for investment products, pushing back the consultation on the proposals.

The FCA said it had postponed this until the autumn to allow it to take into account other international policy initiatives. It is likely that the main developments that FCA is looking at are the ones coming from the International Sustainability Standards Board, which is currently consulting on two exposure drafts on sustainability and climate disclosures. The deadline for the ISSB consultation is set for the 29th July.

Update to the UK Green Finance Strategy

On 12 May 2022, the UK Government published a Call for Evidence to support the development of an update to the UK's Green Finance Strategy.

The Green Finance Strategy, which was published in July 2019, aimed to green financial systems and mobilise finance for clean and resilient growth. This Call for Evidence seeks views and evidence from stakeholders to support the Government in developing an update to the 2019 strategy so the UK can better ensure the financial services industry is supporting the UK's energy security and its climate and environmental objectives. The consultation closed on 24 June, and the updated strategy is planned for publication in late 2022.

European Sustainability Reporting Standards

The European Financial Reporting Advisory Group (EFRAG) launched the draft of its Sustainability Reporting Standards (ESRS) for consultation. The draft published standards are currently sector-agnostic, and cover a number of areas including:

- ESRS 1: General Principles

- ESRS 2: General Strategy, Governance and Materiality Assessment Disclosure Requirements

- ESRS E1: Climate Change

- ESRS E2: Pollution

- ESRS E3: Water and Marine Resources

- ESRS E4: Biodiversity and Ecosystems

- ESRS E5: Resource Use and Circular Economy

- ESRS S1: Own Workforce

- ESRS S2: Workers in the Value Chain

- ESRS S3: Affected Communities

- ESRS S4: Consumers and end-users

- ESRS G1: Governance, Risk Management and Internal Control

- ESRS G2: Business Conduct

The plan is to publish the final sector-agnostic standards in November 2022. They will be followed by a set of sector-specific disclosure standards, expected in 2023.

Updated Supervisory Statement on the Application of the SFDR

In late March the European Supervisory Authorities updated their joint supervisory statement on the application of the Sustainable Finance Disclosure Regulation (SFDR). This included a new timeline, expectations about the explicit quantification of the product disclosures under Article 5 and 6 of the Taxonomy Regulation, and the use of estimates.

The ESAs recommend that national competent authorities and market participants use the current interim period from 10 March 2021 until 1 January 2023 to prepare for the application of the forthcoming Commission Delegated Regulation containing the Regulatory Technical Standards (RTS) while also applying the relevant measures of SFDR and the Taxonomy Regulation according to the relevant application dates outlined in the supervisory statement.

Corporate Sustainability Reporting Directive

On 22nd June 2022 the European Parliament and Council reached a provisional agreement on the text of the Corporate Sustainability Reporting Directive. The regulation includes:

- Extended scope of the CSRD requirements to all large public-interest undertakings as defined by the Accounting Directive and all large undertakings and undertakings that are listed on regulated markets in the EU (including all listed SMEs, but not micro entities). Certain third-country (non-EU) undertakings "generating a net turnover of EUR 150 million in the EU and which have at least one subsidiary or branch in the EU" should also provide sustainability information (see below).

- Updated and new reporting requirements on sustainability matters (such as environmental rights, social rights, human rights, work ethics and governance factors) and the process used to identify this information, using sustainability reporting standards developed by the European Financial Reporting Advisory Group (EFRAG).

- Audit and certification requirement for sustainability reporting to be provided by an accredited independent auditor (either the statutory auditor or another statutory auditor) or a certifier, and assurance to be obtained also on reporting by non-EU companies.

- Requirement to report as from:

- 1 January 2024 for companies already subject to the EU non-financial reporting directive;

- 1 January 2025 for companies that are not presently subject to the EU non-financial reporting directive but fall within the CSRD's enlarged scope;

- 1 January 2026 for EU listed SMEs, EU small and non-complex credit institutions and captive insurance undertakings, and if opt-out as from 1 January 2028 for SMEs

- 1 January 2028 for non-EU companies

Once ready and translated, EU Member States will have 18 months to transpose the CSRD into their national rules. For non-EU companies listed on EU regulated markets, it is expected that the requirements will be effective from 1 January 2025.

For other non-EU companies (referred to as third country undertakings in the Regulations), the requirement to provide a sustainability report applies from 1 January 2028 to all third country undertakings generating a net turnover of more than €150 million in the EU, and which have at least one large or listed EU subsidiary or an EU branch generating a net turnover of more than €40 million.

It will be the EU subsidiary or EU branch of the non-EU undertaking that is responsible for publishing the sustainability report of the third country undertaking. The specific information required to be in these sustainability reports has not been finalised. The Regulation says it should be prepared in accordance with "standards to be adopted by 30 June 2024 by the EC". There will also be the option to report in accordance with the EFRAG sustainability standards or standards which are deemed equivalent. What may be deemed 'equivalent' is yet to be determined by the Commission.

Nuclear and Natural Gas Included in the EU Taxonomy

After initially signalling that nuclear and gas activities would not be included in the text of the European Taxonomy, on Wednesday 6 July the European parliament rejected a motion to oppose the inclusion of nuclear and gas as environmentally sustainable economic activities.

The new rules will add gas and nuclear power plants to the EU "taxonomy" rulebook from 2023, enabling investors to label and market investments in them as green. The Taxonomy Delegated Act will enter into force and apply as of 1 January 2023. Luxembourg and Austria said they would challenge the law in court.

Task Force for Nature Related Financial Disclosures

In late June the Taskforce for Nature-Related Financial Disclosures (TNFD) published for consultation a new Beta 2.0 version of its proposed framework. The second iteration includes several additional elements, including:

- A draft architecture for metrics and targets and an illustrative set of assessment metrics to support pilot testers;

- Further guidance on how to undertake dependency and impact evaluation as well as the identification of priority locations as part of its 'Locate/Evaluate/Assess/Prepare' (LEAP) approach for nature-related risk and opportunity management;

- An overview of the Task Force's approach to the future development of additional guidance for market participants, including sector classification aligned with the approach taken by the International Sustainability Standards Board (ISSB), the Sustainability Accounting Standards Board (SASB) and the Task Force on Climate-related Financial Disclosures (TCFD);

- Enhancements to the LEAP approach for financial institutions (LEAP-FI) first released in March; and

- Additional practical guidance for market participants interested in starting to pilot test the beta framework from 1 July 2022 to 1 June 2023.

The consultation is currently ongoing and the final framework is expected to be published around September 2023.